2 Key Reasons Suggest Dollar Will Be Stronger Than Euro">

2 Key Reasons Suggest Dollar Will Be Stronger Than Euro">

2 Key Reasons Suggest Dollar Will Be Stronger Than Euro

The US economy continues to exhibit robust job growth. This development provided a glimmer of hope for a potential interest rate cut in June, which set a potential bull case for the US dollar.

Solid US jobs data

The unemployment rate declined to 3.8%, meeting market expectations. Employment surged by 303,000 jobs in March, surpassing February's 270,000 job additions and significantly exceeding the anticipated 200,000. Key sectors such as healthcare and government continued to expand their workforce, alongside more cyclical sectors like construction, retail trade, and hospitality and leisure.

Despite the impressive job figures, they may not necessarily bolster the case for an immediate reduction in interest rates by the Fed. On this Wednesday, attention is likely to be focused on the US inflation data for March. The US inflation figures for March are anticipated to garner significant interest due to their role in determining the possible initiation of interest rate cuts by the Fed. This interest is heightened following recent conflicting statements from policymakers.

Fed Chair Jerome Powell recently indicated that interest rate cuts remain probable later this year despite the robust state of the economy. Specifically, he noted that the stronger-than-anticipated inflation figures for January and February have not altered the Fed's policy stance. However, Neel Kashkari, President of the Federal Reserve Bank of Minneapolis, expressed reservations about potential rate cuts should inflation persist at its current level. His comments suggest that the inflation data will be subjected to rigorous scrutiny, particularly in light of the recent uptick in crude oil prices.

ECB meeting might offer hint on rate cut

Another focus this week is the European Central Bank’s meeting. The falling levels of inflation mean it could discuss interest-rate cuts actively for the first time and set the stage for a possible rate cut in June.

The minutes of the latest ECB meeting said the Governing Council would have “significantly more data and information” by the June meeting, especially on wage dynamics, while the new information available in time for the April meeting would be “much more limited, making it harder to be sufficiently confident about the sustainability of the disinflation process by then.”

Overall, the recent weak economic data from the eurozone, coupled with diverging monetary policy expectations between the ECB and the Fed, suggest a possible downward trajectory for the EUR/USD exchange rate in the near term.

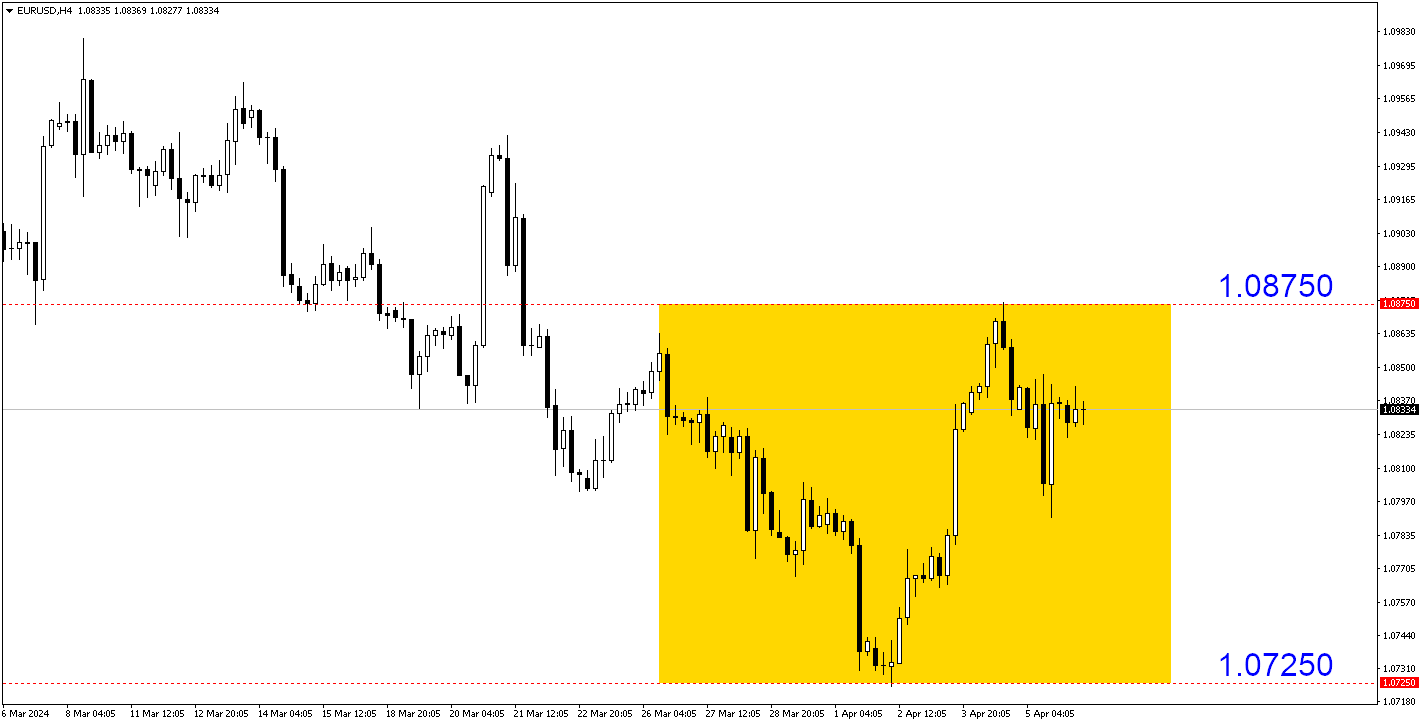

EUR/USD (H4): Being rejected from a Resistance level at 1.08750, the pair is likely heading back near Support level at 1.072500.

Fullerton Markets Research Team

Your Committed Trading Partner